What do you think of when you hear the phrase "financial plan"?

Is it something tangible, like a 60-page document with boring charts and graphs?

Or maybe it's a series of strategic decisions you plan to make that live inside your brain.

The reality is that a financial plan can mean so many different things that the term almost has no universal meaning.

If you're looking for a formal definition of a financial plan, it may look something like this:

Financial Plan Defined

A financial plan is a comprehensive strategy designed to help you manage your finances in a way that aligns with your personal goals and circumstances. It serves as a roadmap for achieving both short-term and long-term financial objectives, providing a structured approach to handling money effectively. A financial plan typically includes:

Assessment of Current Financial Situation: This involves evaluating your income, expenses, assets, and liabilities. Understanding where you stand financially is essential for setting realistic goals and creating a workable plan.

Goal Setting: The plan outlines your financial goals, which could range from saving for retirement, buying a home, or funding education, to managing debt or building an emergency fund. Goals can be short-term (like saving for a vacation) or long-term (such as retirement planning).

Budgeting: A detailed budget is often a core component of a financial plan. It helps you track your income and expenses, ensuring that you live within your means and allocate funds appropriately to meet your goals.

Investment Strategy: Based on your risk tolerance, time horizon, and financial goals, the plan includes recommendations for investments. This might involve choosing among stocks, bonds, mutual funds, real estate, or other investment vehicles.

Debt Management: The plan addresses strategies for managing and reducing debt such as creating a debt repayment plan or consolidating loans, to improve your overall financial health.

Insurance and Risk Management: To protect yourself and your assets, the plan evaluates your insurance needs. This might include health insurance, life insurance, disability insurance, and property insurance, ensuring you are adequately covered against potential risks.

Tax Planning: The plan includes strategies to minimize your tax liability. This involves understanding how different financial decisions impact your taxes and using available tax-saving opportunities such as deductions and credits.

Retirement Planning: This component focuses on saving and investing for retirement, determining how much you need to save, and choosing appropriate retirement accounts and investment strategies.

Estate Planning: For those concerned with passing on assets, the plan includes strategies for estate planning such as creating wills, trusts, and other legal documents to ensure your assets are distributed according to your wishes.

Regular Review and Adjustment: A financial plan is not static. It requires regular reviews and updates to reflect changes in your life circumstances, goals, and financial situation.

Key Takeaways

A financial plan:

Provides a structured approach to managing your money.

Offers guidance to help you make informed decisions, stay organized, and work towards achieving your financial goals.

Must be regularly reviewed and updated as needed.

To make it easier to digest what a financial plan is and, more importantly, the value of having one, I'm going to share a One-Up Financial plan example from start to finish, including the steps our firm takes in preparing a financial plan along with screenshots from the plan itself.

Please note that the information provided below is based on a hypothetical client scenario and is used for illustrative purposes only. Further, return assumptions used in the financial plan are based on historical market data and do not guarantee future results.

Let's get started!

One-Up Financial Planning Step 1: Get to Know Our Client

Before we dive into the sample financial plan, we have to understand the unique circumstances of our client.

👉 One of the first steps in our financial planning process at One-Up Financial is getting to know our clients.

Not just how much money they make or what's in their bank accounts (though both are important), but understanding their financial goals, their family dynamic, and what they value most.

Meet the McFlys!

The new clients we'll be creating a financial plan for are Marty and Jennifer McFly.

Marty and Jennifer are in their mid-50s and live in Hilldale, CA. They have two teenage children, Marty Jr. and Marlene, who plan to attend college in the next few years.

Marty is the CEO of his dad's publishing company and Jennifer owns her own consulting business. Their household income is above $300,000, and they each contribute the maximum to their retirement plans each year. Their total retirement asset balance is $2 million.

Marty hit it big a few years ago betting on a horse race. Accordingly, the McFlys have a large portion of money sitting in a brokerage account, taking their net worth to over $5 million.

They own their home along with a mortgage that's set to be paid off in 10 years, which would leave them debt-free.

Their previous advisor, Biff, hasn't been providing the level of service Marty and Jennifer are looking for from a financial planning perspective, and they're concerned about hidden fees within their investments and whether they are paying too much in taxes.

Now that we have a better understanding of the McFlys financial situation, the next step in creating the financial plan is to establish and prioritize financial goals so we know what we're working towards.

✅ Goal 1: Early Retirement

Marty and Jennifer have made it abundantly clear that they want to be done working at 63, though they would love to retire sooner if possible so long as they can comfortably afford their current lifestyle while being able to travel the world in their DeLorean. This is their primary goal as they value their time and experiences with family and friends above all else.

✅ Goal 2: College Funding

In addition to an early retirement, the McFlys would also like to fund their kids' college tuition. Marty, Jr. plans to attend a local college while Marlene has her heart set on Penn State. The estimated total tuition costs are $90,000 per year.

✅ Goal 3: Home in Florida

If early retirement can be achieved along with funding their kids' college tuition, Marty and Jennifer would like to purchase a home in Florida and establish residency to help save on state taxes. They met with a realtor and the homes they're targeting are in the $1.5 million range.

✅ Goal 4: Home Remodel and Donations

Lastly, Marty expressed interest in helping fund the rebuild of the Hill Valley Clock Tower after it was struck by lightning, in addition to gifting to other charities. Jennifer also wants to remodel the kitchen.

One-Up Financial Planning Step 2: Gather and Input Data

With financial goals now established and prioritized, we then need to gather the financial data necessary to start building the financial plan.

At the very least, this includes requesting the following details:

Ages of all family members

Copy of their most recent tax return

Copies of all investment statements

Listing of all assets and values, i.e. bank accounts, real estate, business ownership

Listing of all liabilities, i.e. credit card debt, mortgage balance (with rate and amortization)

Social security estimates

Copies of insurance policies

Copies of their estate plan including wills, trusts and medical directives

Once the McFlys have uploaded all of this information to their secure digital storage vault within their One-Up Financial online financial planning portal, we then input the data into our financial planning software and review to ensure we've accounted for everything.

After a thorough review is complete, a "blueprint" is created to make it easier for our clients to visualize their net worth (assets less liabilities), financial goals, and income/savings/expenses, a.k.a cash flow statement.

Sample: Net Worth Blueprint

The net worth blueprint is essentially a balance sheet, including our clients' current cash position, retirement accounts, mortgage balance and any other assets/debts of the family household. This financial statement is a good indicator of one's overall financial health.

Sample: Financial Goals Blueprint

Note that in addition to accounting for the McFlys goals within their financial plan, we also plan for unexpected costs that may arise in retirement, such as long-term care expenses.

Sample: Income, Savings and Expense Blueprint, a.k.a. Cash Flow Statement

Sometimes referred to as a cash flow statement, this is an important financial planning tool for visualizing household cash inflows and outflows.

One-Up Financial Planning Step 3: Analyze the Data

After sharing the financial blueprints with the McFlys and verifying all of their information is accurately reflected, the next step in the financial planning process is analyzing the data.

During this step, our goal is to accomplish three things:

Identify opportunities to optimize our clients' finances and save them money now and in the future.

Detect risk and errors resulting from misalignment when comparing our client's financial data with their goals and objectives.

Establish multiple "what-if" scenarios to plan for best- and worst-case future financial outcomes in retirement.

💰 Optimizing Finances and Saving Money

In analyzing the McFlys' data, we uncovered Marty and Jennifer's joint taxable brokerage account was invested in mutual funds, most of which had 12b-1 fees, high expense ratios and large unrealized losses.

By rebalancing out of these mutual funds and into low-cost index funds, we estimate the McFly's can save as much as $14,000/year in fees and taxes.

On top of the savings from the brokerage account, we noticed Marty wasn't taking advantage of the $1,000 health savings account (HSA) employer match offered through work as he wasn't actively contributing to his HSA. By maxing out his family HSA, Marty and Jennifer stand to save $1,400/year.

Lastly, we noted the McFlys have equity in their home and brokerage account without any lines of credit established. Accordingly, we're recommending they consider opening a home equity line of credit and a line tied to their investments, otherwise known as a securities-based line of credit to further enhance their access to liquidity, especially considering their goal of purchasing a home in Florida.

⚠️ Risks and Errors

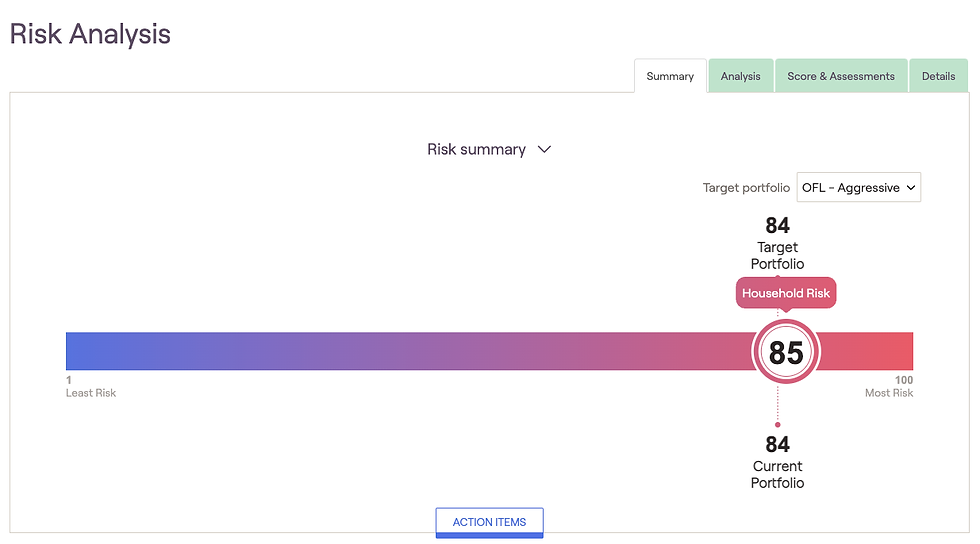

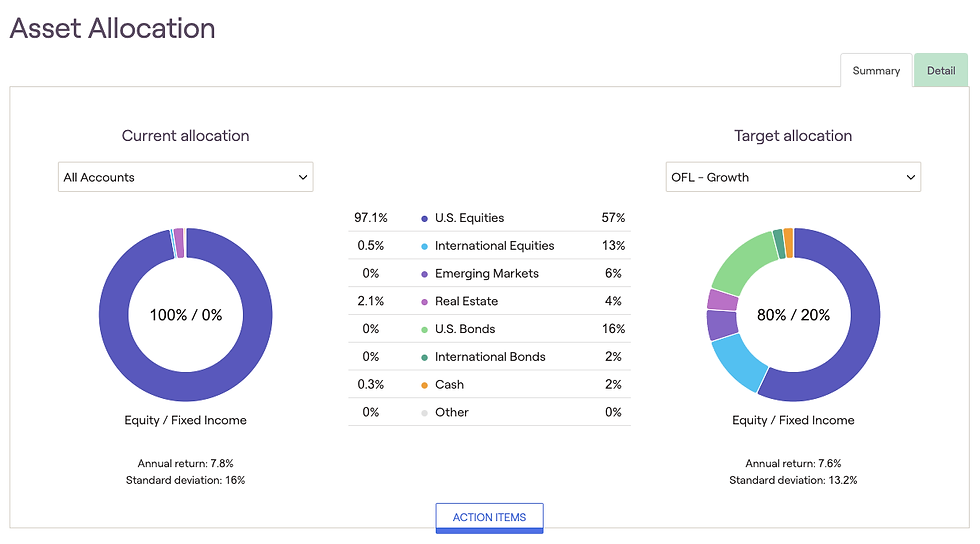

Continuing with our analysis, we reviewed Marty and Jennifer's answers to the risk tolerance questionnaire to help determine their optimal asset allocation across their investments.

Upon review, we noted their "risk score" is 85, meaning they're both willing to take risk in the market, but also prefer to have some downside protection.

We compared their risk score to their current allocation which was considerably more aggressive and almost fully concentrated in large-cap growth stocks. Clearly, Biff wasn't doing his job!

In addition to the opportunity for rebalancing their portfolios and reducing equity risk to more closely resemble their risk score, we noticed the McFlys previous accountant failed to claim various tax credits including the electric vehicle tax credit on their prior years' tax return which would have reduced their tax liability by $3,500. Accordingly, we'll be recommending they amend their tax return.

🤔 What-If Scenarios

After identifying every possible way to save the McFlys money and resolve discrepancies between the data and their goals, we then wanted to get creative! By that, I mean we take the information gathered thus far and brainstorm a variety of scenarios that would help our clients exceed their financial goals without compromising their probability of success, i.e. the likelihood of their money lasting long into retirement. We call these "stretch goals."

For example, we considered:

What if Marty and Jennifer retired 5 years earlier than planned?

What if the McFlys took less risk in the market?

What if the McFlys wait to take their social security at full retirement age?

What if we implemented a "guardrails" spending strategy in retirement with parameters based on market performance as opposed to the inflation-adjusted approach?

We then look at how those what-if scenarios impact the success rate of their financial plan.

Thankfully, we're happy to report that the McFlys will be able to retire much sooner than they initially hoped, with potentially more wiggle room for implementing additional stretch goals to their financial plan!

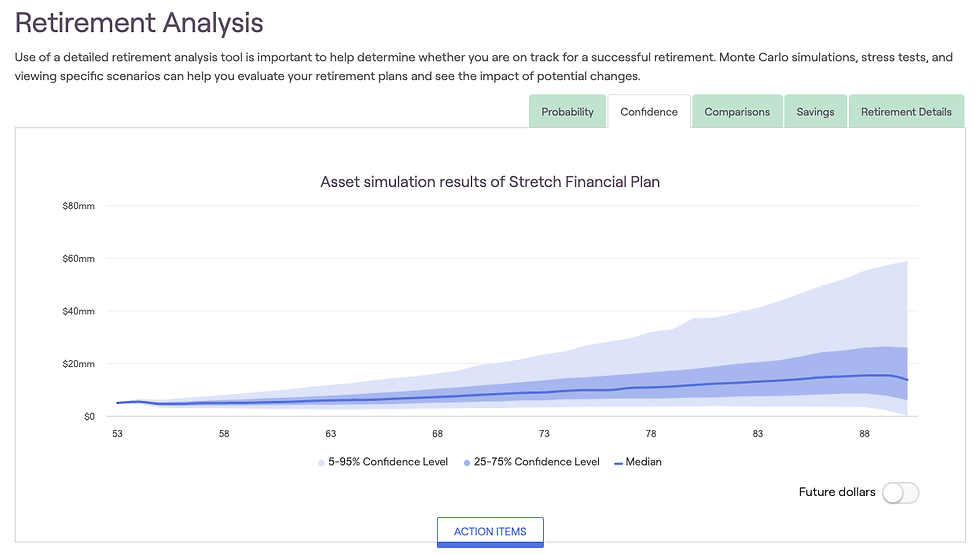

Finally, we simulate the future values of their investments over time, which helps when evaluating our clients' estate plan, something the McFlys have yet to update which, based on our analysis, could end up costing them thousands in estate tax if not done correctly!

One-Up Financial Planning Step 4: Build the Financial Plan

With our analysis and recommendations now complete, the next step is to put everything together into one cohesive presentation and deliver it to our clients.

One of the ways we do this is through our "snapshot" where we capture the most critical components of the financial plan on a single page.

For Marty and Jennifer, the important elements we wanted front and center were:

An action plan of our recommendations, estimated savings from implementing said recommendations, and what to do next.

A breakdown of their net worth, liquidity, savings and tax rate.

Their risk score and a stress test showing potential risks to their financial plan.

On top of our snapshot, we felt the McFlys would benefit from implementing Roth conversions in retirement along with a strategic distribution strategy resulting in an estimated lifetime savings of more than $1.1M.

With the financial plan now fully built, we presented our findings to Marty and Jennifer who were thrilled with our attention to detail, not to mention the results.

One-Up Financial Planning Step 5: Review, Monitor and Update the Financial Plan

After going through every element of the financial plan with Marty and Jennifer and assisting them in implementing the recommended action items, we emphasized the fact that our work has only just begun!

No financial plan is complete without ongoing monitoring and maintenance.

The reality is that change is constant and inevitable.

That Florida home the McFlys have dreamt of for years may instead have to be in South Carolina so they can be closer to their kids and grandkids.

The 5% yield Marty and Jennifer were getting in their high-yield savings account has quickly dwindled to 2%, causing them to rethink their investment strategy.

Plans change. So does the stock market and the economy.

Failing to account for an ever-changing environment will result in an out-of-date financial plan that can lead to costly financial mistakes down the line. Thankfully, the McFlys have engaged One-Up Financial as their trusted financial advisor to proactively review and update their plan.

Review Meetings

While no financial plan is the same from one person to the next, most financial planning engagements involve frequent check-in meetings whether in-person, over the phone or via Zoom. The number and frequency of meetings vary based on client preference.

💪 At One-Up Financial, we recommend a minimum of three financial planning meetings per year, though encourage more as we're big on communication!

The Role of a Financial Professional

Creating, monitoring, and updating a financial plan is a daunting task most people prefer outsourcing to a financial professional.

Financial advisors come in all shapes and sizes, thus it's important to choose your financial advisor wisely and focus on those who've obtained the Certified Financial Planner (CFP) designation and ones with experience working with clients like yourself. I created a guide to helping investors find a qualified, fiduciary financial advisor which can be found here.

A good financial planner will review your portfolio several times each year and provide investment advice only.

An exceptional advisor will invest time to understand your unique financial situation and work hard to proactively help you financially adapt with ease and confidence to the inevitable changes life throws at you. With One-Up Financial, a CFP who is also a Certified Public Accountant (CPA) brings an added bonus to clients as we know where, and how to uncover tax advantages other advisors miss.

After completing the financial plan for Marty and Jennifer and engaging with them quarterly to provide updates, we're confident they can now sleep better at night knowing they have a comprehensive financial plan that will help them achieve long-term financial stability and security.

toto togel adalah platform pusat online yang menawarkan pengalaman bermain yang seru dan mengasyikkan

Raja288 , Slot Online , Slot Gacor , Raja288 , Slot Thailand , Slot Server Thailand , Raja288 , Judi Bola , Judi Bola Online , Raja288 , Casino Online , Raja288

KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO VERTU789 VERTU789 KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO KARATETOTO

Situs Toto

Situs Togel

Togel

Toto Slot

Situs Toto

Situs Togel

Toto Slot merupakan link bermain situs judi online berlisensi resmi aman dan terpercaya

Situs Toto

Situs Togel

Toto Slot

Main situs togel terpercaya dengan 3 link rekomendasi terbaik hari ini